AI/실습

[Python] LSTM을 이용한 주가 예측

쏘니(SSony)

2023. 1. 10. 14:11

LSTM의 구조 및 특징

1. RNN에 비해 무한대의 기억 능력

2. RNN의 gradient 문제 극복

3. Momory Block 구조

- sigmoid 함수 계열의 activation function이 사용됨 (hard sigmoid를 사용하면 성능 UP)

- output을 만들 때는 tanh 함수 사용

LSTM 기반 주가 예측

- 주가는 정상성을 만족하지 않음

- 수익률 자체도 정상성을 만족하지는 않음 ( ← 수익률 평균이 일정하지 않으므로)

⇒ 비정상성 제거 후 예측 진행

- EMA(Exponential Moving Average) 이용

import yfinance as yf

import pandas as pd

import numpy as np

import talib# 데이터 다운로드

start = '2017-12-16'

end = '2022-12-15'

KOSPI = yf.download('^KS11', start, end) #KOSPI index보통 6년치 데이터 다운로드 받음 (train : 5년, test : 1년)

KOSPI.head()

# 조정 종가 사용

kospi = KOSPI['Adj Close']

# 수익률과 비슷한 데이터 생성

kospi = np.log(kospi) - np.log(talib.EMA(kospi, 10))10일치 EMA를 통해 최근 지수를 반영한다.

from statsmodels.graphics.tsaplots import plot_pacf

plot_pacf(yt, lags=40, method='ols', title='Partial Autocorrelation').show

하늘색으로 색칠된 부분은 신뢰구간

p = 3 일 때 구간 밖으로 나와있음 (뒤에 몇개 구간 밖에 것들은 노이즈로 취급)

→ p = 3으로 결정

yt_1 = yt.shift(1) # 1일 전 adjusted kospi

yt_2 = yt.shift(2) # 2일 전 adjusted kospi

yt_3 = yt.shift(3) # 3일 전 adjusted kospi

data = pd.concat([yt, yt_1,yt_2,yt_3], axis=1)

data.columns = ['yt', 'yt_1', 'yt_2', 'yt_3']

data = data.dropna()

data.head()

# 주가 예측을 위한 종속변수 및 독립변수 지정

y = data[['yt']]

x = data[['yt_1', 'yt_2', 'yt_3']]#pip install sklearn

#!pip install scikit-learn

from sklearn import preprocessing

num_attrib =3

scaler_x = preprocessing.MinMaxScaler(feature_range = (-1, 1))

x = np.array(x).reshape((len(x), num_attrib))

x = scaler_x.fit_transform(x)

num_response = 1

scaler_y = preprocessing.MinMaxScaler(feature_range = (-1 , 1))

y = np.array(y).reshape((len(y), num_response))

y = scaler_y.fit_transform(y)# train : 전체 데이터의 80%, test : 20%

train_end = int((x.shape[0]*0.8))

x_train = x[0:train_end, ]

x_test = x[train_end:data_end, ]

y_train = y[0:train_end]

y_test = y[train_end:data_end]

# 2차원 -> 3차원으로 reshape for LSTM

x_train = x_train.reshape(x_train.shape[0], 1, x_train.shape [1])

x_test = x_test.reshape(x_test.shape[0] , 1, x_test.shape [1])

print(" Shape of x_train is ", x_train.shape)

print(" Shape of x_test is ", x_test.shape)#!pip install keras

#!pip install tensorflow

from keras.models import Sequential

from keras.layers.core import Dense, Activation

from keras.layers import LSTM

#from keras.layers.recurrent import LSTM

seed = 2016

np.random.seed (seed)

fit1 = Sequential()

fit1.add(LSTM(units = 4, # 수정가능

activation = 'tanh',

recurrent_activation = 'hard_sigmoid',

input_shape =(1, 3)

)

)

fit1.add(Dense(units = 1, activation = 'linear'))fit1.compile (loss ="mean_squared_error", optimizer ="rmsprop") # Root Mean Sqaure Propagation

fit1.fit(x_train, y_train, batch_size =1, epochs =10, shuffle = True)

print(fit1.summary())

- 시계열 데이터를 3단위로 잘라 input으로 넣음

- 훈련이 3단위로 이루어짐 : 각 단위 내에서는 시계열로 이루어져있음

- shuffle을 해도 문제 없음, 성능이 더 높아짐

score_train = fit1.evaluate(x_train, y_train, batch_size =1)

score_test = fit1.evaluate(x_test, y_test , batch_size =1)

print ("in train MSE = ", round(score_train, 4))

print ("in test MSE = ", round(score_test, 4))train MSE : 0.0064

test MSE : 0.0063

=> MSE 가 아주 작음

pred=fit1.predict(x_test)

pred1=scaler_y.inverse_transform(np.array(pred).reshape((len(pred),1)))

y_test1=scaler_y.inverse_transform(np.array(y_test).reshape((len(y_test),1)))

%matplotlib inline

import matplotlib.pyplot as plt

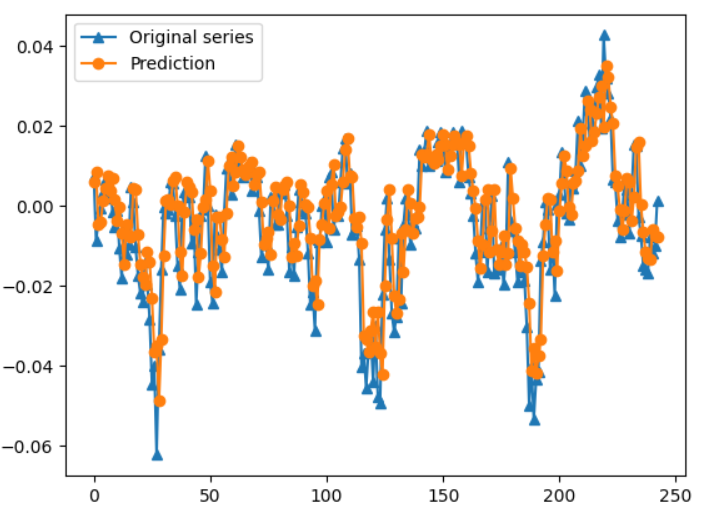

plt.plot(y_test1, marker = '^', label = "Original series")

plt.plot(pred1, marker = 'o', label = "Prediction")

plt.legend()

두 그래프가 거의 유사 : 예측 성공

본 자료는 중앙대학교 블랙스톤 금융AI 아카데미 (Blackstone Financial AI Academy) 코딩 부트 캠프 강의 자료를 참고하여 제작하였습니다.